Subscribe

The latest escalation between Iran and Israel is not only a geopolitical event. It is a structural shock to energy-importing economies. For India, the implications run through oil markets, fertiliser supply chains, shipping corridors, public finance and climate commitments. The issue is not whether barrels continue to move. The issue is at what price, under what risk premium and with what policy trade-offs.

In crisis discourse, energy security and climate ambition are frequently framed as competing priorities. The present conflict shows the opposite. Oil import dependence is a macroeconomic vulnerability. Reducing it through electrification, renewable deployment and efficiency gains is both a climate and a security strategy.

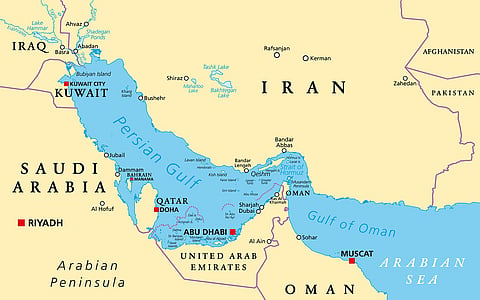

India imports more than 85 per cent of its crude oil. A significant share passes through the Strait of Hormuz, which handles roughly a fifth of global petroleum liquids trade. A sustained increase of even $10 per barrel materially widens the import bill. The current account deficit expands. The rupee faces depreciation pressure. Imported inflation follows through fuel, transport and petrochemicals.

India’s progress in solar and wind capacity expansion has already lowered the carbon intensity of power generation. Yet oil dominates transport and significant segments of industry. Accelerating electric mobility in two- and three-wheelers and public transport directly reduces exposure to crude price volatility. Expanding rail freight share reduces diesel consumption in logistics. These are structural hedges, not long-term aspirations.

In conflict conditions, physical closure of the Strait is only one scenario. More common are anticipatory price spikes driven by insurance costs, tanker rerouting, higher freight rates and speculative positioning in futures markets. Fertilisers become costlier because natural gas and hydrocarbon derivatives underpin urea and other inputs. Agricultural costs rise. Food inflation, already sensitive to climate variability, tightens household budgets across rural India.

Monetary policy becomes reactive. The Reserve Bank of India must weigh supply-driven inflation against growth concerns. Rate hikes to anchor expectations risk dampening investment. Delayed tightening risks price instability. In both cases, the external shock narrows domestic policy space.

The environmental risks of conflict in this region go well beyond price volatility. The Persian Gulf is a semi-enclosed body of water. Its limited water exchange with the open ocean means that pollutants disperse far more slowly than in open sea conditions. A major spill from a damaged offshore platform, a struck tanker or a destroyed refinery facility would spread through shallow coastal waters that support some of the most productive fisheries and mangrove ecosystems in the region.

The 1991 Gulf War provides the clearest precedent. Deliberate releases and combat damage discharged an estimated four to eight million barrels into the Gulf. Recovery of seagrass beds, coral systems and intertidal zones took more than a decade in affected areas and remains incomplete in some. A comparable event under present conflict conditions would affect fishing communities across Kuwait, Bahrain, Qatar, the UAE and Iran’s southern coast.

India’s exposure is indirect but traceable. Indian-flagged vessels and crews operate in West Asian waters. Higher insurance and security costs feed directly into freight rates. When tankers reroute around contested zones, voyage distances increase, raising bunker fuel consumption and shipping emissions. Geopolitical instability therefore increases the carbon intensity of trade even before a single barrel reaches an Indian refinery.

There is a second-order climate effect that receives too little attention. Energy security anxieties routinely trigger renewed investment in upstream oil and gas. Producer states seek to monetise reserves quickly. Importers pursue long-term supply contracts to hedge price risk. These responses lock in fossil infrastructure for decades. For India, which is attempting to reduce emissions intensity while sustaining growth, such lock-in complicates transition planning in ways that are difficult to reverse once contracts and capital commitments are in place.

India’s fuel taxation regime has historically provided fiscal space during periods of moderate oil prices. When global prices rise sharply, governments face a political choice: allow price pass-through and absorb inflationary fallout, or cut excise duties and compress revenue. The latter reduces fiscal headroom for capital expenditure, welfare transfers and climate adaptation spending.

Public sector oil marketing companies often absorb the shock. When retail prices are not fully adjusted, under-recoveries accumulate. These quasi-fiscal liabilities ultimately surface on the sovereign balance sheet. A prolonged conflict therefore does not remain confined to external accounts. It migrates into fiscal sustainability.

This matters directly for environmental governance. India’s nationally determined contribution requires sustained public and private investment in renewable energy, grid expansion, storage and adaptation infrastructure. Elevated oil import bills crowd out that space. The 2022 oil price spike following Russia’s invasion of Ukraine offers a recent data point: central and state governments cut excise on fuel twice within months, reducing combined revenues by an estimated Rs 1 lakh crore. Adaptation and clean energy budget lines face similar pressure in analogous scenarios.

Energy price spikes are regressive. Urban poor households face higher transport fares. Rural cultivators absorb higher diesel and fertiliser costs. Food price inflation erodes real wages. In such contexts, broad fuel subsidies appear politically expedient. Yet they blunt the price signals necessary for efficiency improvement and energy transition.

Targeted income support mechanisms are more consistent with long-term transition goals. India’s direct benefit transfer architecture provides a platform for compensating vulnerable households without distorting market prices. The PM-KISAN scheme and the Ujjwala LPG subsidy model offer templates for delivery at scale. The effectiveness of this approach depends on timely identification of affected households and sustained fiscal capacity to fund transfers.

India has pledged to reduce the emissions intensity of GDP and expand non-fossil power capacity. Meeting these targets in a high-volatility oil environment requires policy coherence across three areas.

First, transition investments must be ring-fenced from fiscal compression. If elevated oil import bills lead to reduced capital expenditure on renewables, grid upgrades or adaptation infrastructure, progress slows precisely when it needs to accelerate. Budget allocations for the National Solar Mission, PM-KUSUM and the Green Hydrogen Mission need protection from discretionary cuts.

Second, adaptation spending deserves equal emphasis to mitigation. Climate impacts in India, from intensifying heatwaves to erratic monsoon patterns, are accelerating. Fiscal compression due to higher oil imports threatens funding for resilient agriculture, watershed management and urban heat infrastructure. The interaction between geopolitical risk and climate vulnerability operates as a compound stress on the same public finance system.

Third, green hydrogen initiatives aimed at fertiliser and refining sectors offer a credible pathway to reducing reliance on imported gas and naphtha. If powered by domestic renewables, hydrogen lowers both import dependence and emissions. Cost competitiveness is not yet established at scale, but the policy case for sustained public investment in demonstration projects and electrolyser manufacturing is strengthened, not weakened, by recurring oil price shocks.

The Iran-Israel conflict exposes a recurring pattern. External geopolitical shocks reveal internal structural dependencies. For India, oil import reliance is not only an energy statistic. It is a macroeconomic, fiscal and environmental variable with measurable consequences for climate governance.

Policy responses that treat the crisis as temporary may stabilise short-term markets but perpetuate structural exposure. Responses that accelerate electrification, diversify energy sources, protect vulnerable households through targeted transfers and maintain fiscal discipline reduce the economy’s sensitivity to future shocks.

Three specific actions follow from this analysis. The Union Ministry of Petroleum should publish a formal assessment of Hormuz-dependent import share and present alternative routing and sourcing options with timelines. The finance ministry should establish a transparent protocol for how fuel excise adjustments interact with transition budget lines, so that price stabilisation does not silently erode clean energy commitments. The Union Ministry of Environment, Forest and Climate Change should incorporate oil price volatility scenarios into its climate finance planning, rather than treating energy markets and climate budgets as separate domains.

Energy security and climate stability are not parallel agendas managed by separate ministries. In a period of sustained geopolitical instability, they require integrated planning and shared fiscal discipline.

Sagari Gupta is a public policy researcher with over eight years of experience in social development, governance reforms, and data-driven policy analysis in India.

Views expressed are the author’s own and don’t necessarily reflect those of Down To Earth